ASX Slides Toward Correction as $250 Billion Wiped Amid Rate Shock Fears

Key Highlights

- ASX loses $250 billion in under three weeks, nearing correction territory

- Interest rate forecasts shift to 4.85% peak, highest since 2008

- Small caps slump -0.85%, signaling risk-off sentiment

- Gold rises above $US4,698, while oil volatility intensifies

- Healthcare stocks emerge as defensive outperformers

A market on edge, and a story still unfolding

The Australian share market is no longer simply reacting to headlines. It is recalibrating.

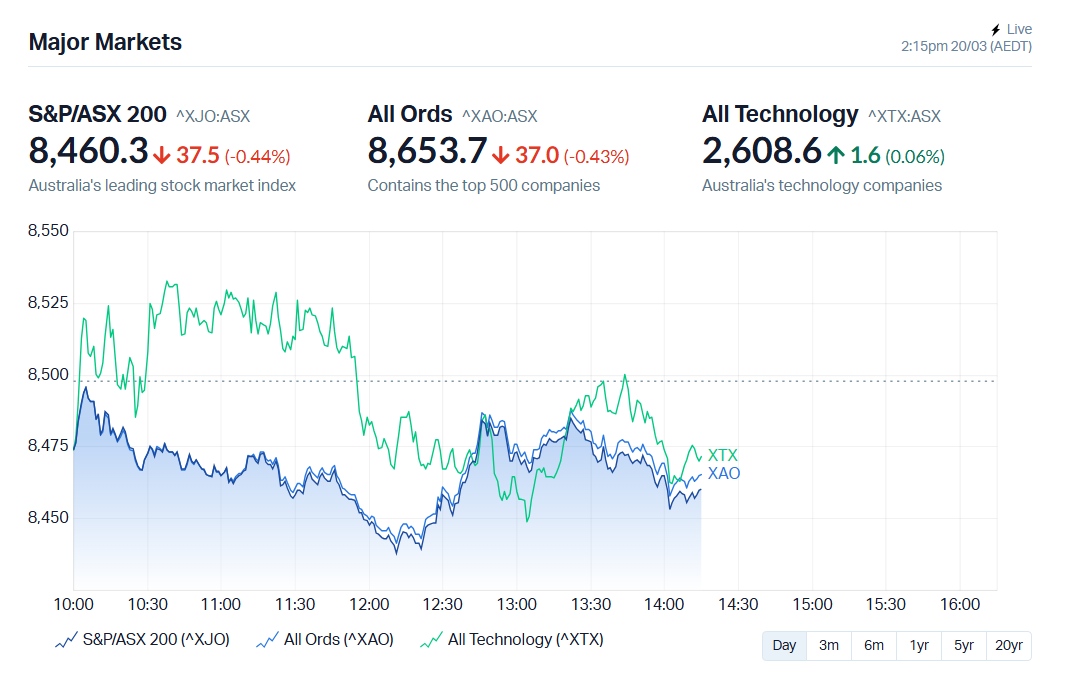

By early afternoon, the ASX 200 had slipped 0.50% to 8,455 points, with the broader All Ordinaries down a similar margin. On the surface, it looked like another modest decline.

But beneath that, a deeper shift is taking place.

Since early March, roughly $250 billion has been wiped from the market, pushing the index close to an official correction. That threshold, defined as a 10% fall from recent highs, is now within reach.

Source: MarketIndex

The “triple hike” fear reshaping sentiment

What began as a geopolitical shock tied to Middle East tensions has evolved into something more structural.

Markets are now grappling with a “hawkish repricing” of global interest rates.

Major central banks, including the US Federal Reserve, the European Central Bank, and the Bank of England, have signalled that inflation remains stubborn. Rate cuts, once expected, are being pushed further out.

Closer to home, forecasts have shifted sharply.

Morgan Stanley now expects three additional rate hikes from the Reserve Bank of Australia in 2026, taking the cash rate to 4.85%, a level not seen since November 2008.

That shift matters because higher rates ripple through everything. Mortgage costs rise, borrowing slows, and company valuations come under pressure.

Already, around 1.4 million Australian borrowers are considered at risk, highlighting the real-world impact of monetary tightening.

Beyond rates: A growing supply shock concern

Adding to the unease is a more complex global risk.

Escalating tensions in the Middle East have reportedly damaged key LNG infrastructure in Qatar, raising concerns not just about energy prices but physical supply.

Research firm BMI has warned that disruptions could extend beyond fuel into agriculture, as gas is a critical input for fertiliser production.

In simple terms, the market is beginning to price in the possibility of higher costs and slower growth at the same time, a scenario often referred to as stagflation.

AMP’s Head of Investment Strategy Shane Oliver captured the mood:

“The most likely scenario right here, right now is that we are in the midst of a correction… possibly of the order of around 15%.”

However, not all economists are convinced the worst is inevitable.

NAB Chief Economist Sally Auld noted:

“Stagflation is one of those scenarios where you have persistently high inflation and a really meaningful lift in the unemployment rate. We are some way away from that outcome.”

Sector divergence tells the real story

The day’s movements revealed a market increasingly divided.

Healthcare led gains, rising 1.58%, with companies like Telix Pharmaceuticals and Sigma Healthcare attracting defensive flows. These sectors tend to perform better when uncertainty rises, as demand for healthcare remains stable regardless of economic cycles.

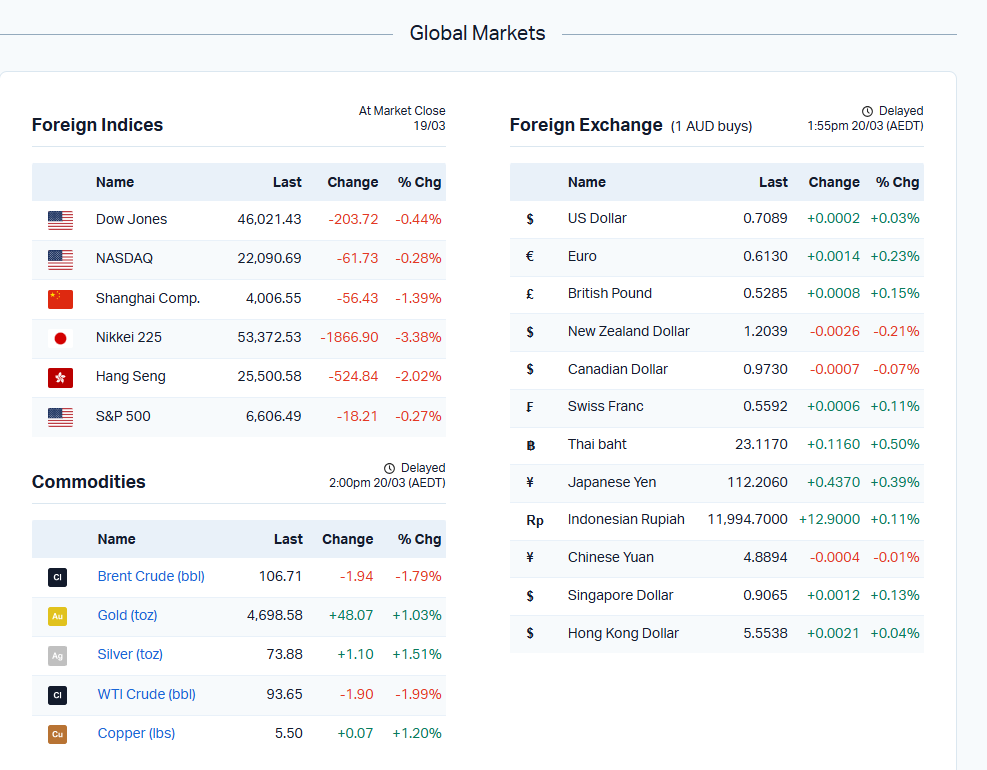

Energy stocks also edged higher, supported by elevated oil prices, even as Brent crude slipped slightly to around $US106 per barrel.

On the other side, the pressure was clear.

Materials dropped sharply, with major miners such as BHP and Rio Tinto declining as commodity prices weakened under a stronger US dollar.

Small-cap stocks were hit hardest.

The Small Ordinaries index fell 0.85%, reflecting a broader retreat from riskier assets. Names like Ora Banda and Bellevue Gold were among those sold off as traders moved away from speculative positions.

Winners, losers, and the shift in behaviour

Among individual stocks, some stood out.

Premier Investments rose more than 6%, showing resilience in discretionary spending, particularly in niche segments like sleepwear and gifting.

Telix Pharmaceuticals climbed over 4%, reinforcing healthcare’s status as a safe haven.

On the downside, Sunrise Energy Metals plunged nearly 18%, while a range of mining and exploration stocks recorded losses between 5% and 10%.

The pattern is familiar in uncertain markets. Capital rotates away from growth and cyclicals into stability.

Global markets echo the caution

Australia is not alone.

Wall Street closed lower overnight, with the S&P 500 and Nasdaq both slipping as investors digested the Federal Reserve’s stance.

European markets fell more sharply, with the FTSE down 2.4% and Euro Stoxx declining 2.3%.

In Asia, China and Hong Kong markets also retreated, while Japan remained closed after a steep sell-off earlier in the week.

The synchronised nature of the decline suggests a coordinated global reassessment of risk.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Source: MarketIndex

Government response and rising stakes

Back home, policymakers are beginning to respond.

Treasurer Jim Chalmers convened a meeting of the Council of Financial Regulators to assess fuel security and economic resilience, highlighting the seriousness of the situation.

The government has also released 762 million litres of fuel from reserves, aiming to stabilise supply concerns.

At the same time, draft electricity pricing proposals suggest potential relief for consumers, with caps expected to fall by up to 10% in some regions.

While positive for households, this may weigh on energy retailers as margins compress.

A market at a crossroads

The ASX now sits at a critical juncture.

With an 8% decline already recorded, the next move will determine whether this remains a short-term correction or evolves into something deeper.

History offers some perspective.

The last comparable period of sustained selling came in mid-2022, when aggressive rate hikes triggered a global equity pullback. Markets eventually stabilised, but only after inflation showed clear signs of easing.

Today’s environment carries similar themes, but with added geopolitical complexity.

For now, the message from the market is clear.

This is no longer just about reacting to news. It is about adjusting to a new economic reality where rates may stay higher, risks are more interconnected, and volatility is likely to persist.

As the ASX edges closer to correction territory, the coming weeks will be crucial in determining whether this is a pause or the start of a more prolonged reset.

Source:ASX Market Data, March 20, 2026; Global market data; AMP, NAB, RBC commentary

What is your take on this story?

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.