Market Wrap: ASX Claws Back Losses After Wall Street Rout as Oil Shock Looms

Key Highlights:

- ASX 200 trims early losses to close around -0.74% at 8,366 points

- Wall Street sell-off spills into Asia amid geopolitical tensions

- Brent crude holds above $112, fuelling inflation concerns

- Energy and defensives outperform while miners and small caps slide

- Analysts warn oil shock could reshape global growth outlook

A market caught between panic and resilience

Australian share market began the week on shaky ground, but by the afternoon, it showed signs of composure.

After plunging early in the session, the ASX 200 managed to claw back some losses, closing down 0.74% at 8,366 points, a far more measured decline than what the morning had suggested.

Source: MarketIndex

The trigger was not local.

It rarely is in moments like this.

Instead, the tone was set thousands of kilometres away on Wall Street, where a sharp sell-off on Friday reflected growing anxiety around geopolitics, oil prices, and the trajectory of global interest rates.

The global backdrop: a market on edge

The selling pressure came after a turbulent session in the United States.

The S&P 500 fell 1.51%, the Nasdaq dropped 2.01%, and the Dow Jones slid nearly 1%. It marked the third consecutive losing session for US equities.

At the heart of the volatility is a rapidly escalating situation in the Middle East.

Market analyst Tony Sycamore described it bluntly:

“President Trump’s threat has now placed a 48-hour ticking time bomb of elevated uncertainty over markets. If the ultimatum is not walked back before the re-open, we will likely see global equity markets extend falls as oil prices spike again.”

That uncertainty is now filtering directly into global markets.

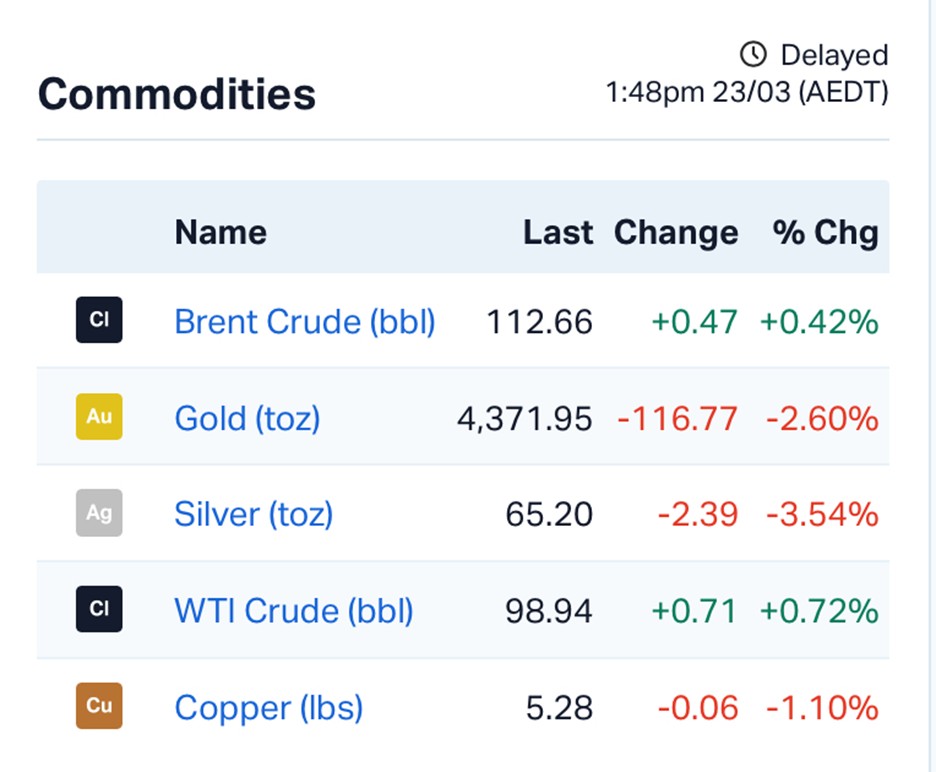

Oil shock fears begin to bite

Brent crude is hovering around $112 per barrel, a level that immediately raises concerns about inflation and economic growth.

Source: MarketIndex

History offers a sobering comparison.

Oil shocks in 1973 and 1979 triggered prolonged economic slowdowns, with ripple effects felt across global markets for months.

Shane Oliver, Head of Investment Strategy at AMP, pointed to a similar risk emerging:

“The war could still go on for many weeks yet and see oil prices rise, say, to $US150 a barrel. Past oil shocks unfolded over many months. The steady destruction of energy infrastructure means it will take longer to get supply back to normal.”

For markets, the implication is clear.

Higher oil prices do not just mean expensive petrol. They translate into higher costs across transport, manufacturing, and food production.

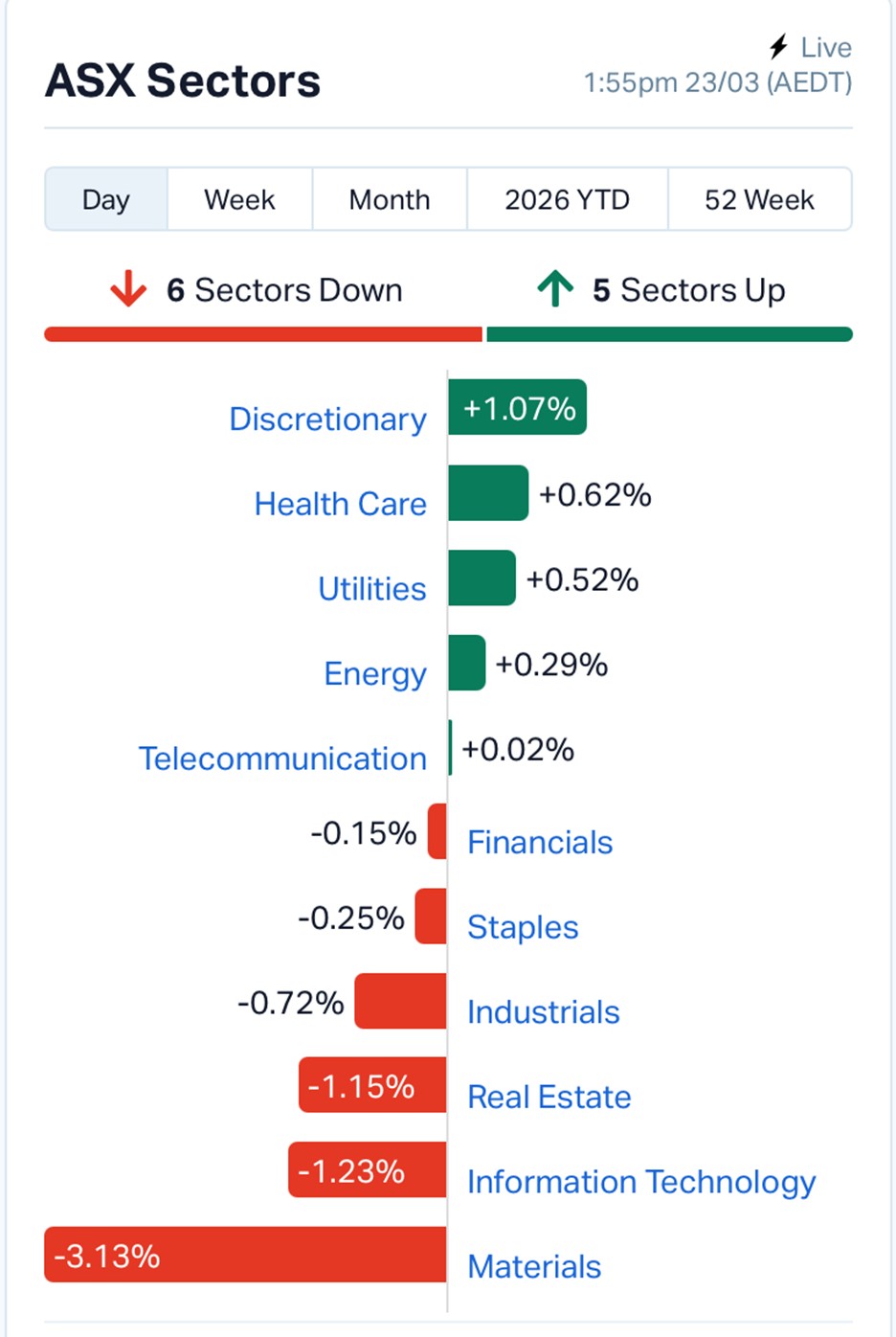

ASX performance: resilience beneath the surface

Despite the heavy global backdrop, the ASX showed relative resilience compared to its Asian peers.

While Japan’s Nikkei plunged more than 3% and South Korea’s Kospi fell sharply, Australia’s losses remained contained.

Still, the divergence within the market was striking.

Winners

Energy stocks held firm, supported by rising crude prices. Companies like Viva Energy and Karoon Energy tracked oil higher, offering a rare pocket of strength.

Healthcare and utilities also attracted buyers, reflecting a shift toward defensive sectors.

Losers

Materials stocks bore the brunt of the sell-off. The ASX 200 Resources index dropped 2.46%, as fears of slowing global demand weighed on metals like copper.

Daniel Hynes, Senior Commodities Analyst at ANZ, explained the pressure:

“Copper led the base metals sector lower amid the broad selloff as the Middle East conflict stokes concerns about inflation and economic growth. Higher prices for energy will hurt manufacturing and economic activity worldwide.”

Gold miners also fell sharply, with the gold sub-index down more than 7%, despite bullion traditionally being seen as a safe haven.

Small caps feel the heat

If large caps showed resilience, smaller companies told a different story.

The Small Ordinaries index dropped 1.95%, reflecting a clear risk-off sentiment.

Stocks such as Atlantic Lithium fell more than 15%, leading a broad sell-off in speculative names.

This pattern is familiar.

In times of uncertainty, capital tends to rotate away from higher-risk segments and into more stable, cash-generating businesses.

The currency and rates story

The Australian dollar weakened to 0.6994 US cents, reflecting both global risk aversion and expectations of tighter monetary policy.

Stay ahead of the market

The most important stories, delivered to your inbox. No noise, just what matters.

By subscribing, you agree to our Privacy Policy.

Markets are increasingly pricing in further rate hikes from the Reserve Bank of Australia.

Economist Ben Jarman from J.P. Morgan highlighted the broader impact:

“These downgrades are based largely on local factors, with some reinforcement by the inflation element of the oil shock. Growth will be more restrained in 2026 given the interest rate outlook, compounding consumer moderation.”

This combination of slowing growth and persistent inflation has revived discussions around stagflation, a scenario markets are keen to avoid.

What comes next

The coming days will be critical.

Investors are watching three key developments.

First, Australia’s upcoming inflation data will offer insight into whether price pressures are easing or accelerating.

Second, geopolitical developments around key oil supply routes remain front of mind. Any escalation could push crude prices even higher.

Third, central bank commentary will shape expectations around interest rates, particularly as markets reassess how long policy will remain restrictive.

A market adjusting to a new reality

For now, the ASX appears to be navigating a delicate balance.

On one hand, global uncertainty is rising, driven by geopolitical tensions and energy market disruptions.

On the other, there are signs of resilience, particularly in sectors that benefit from higher commodity prices or offer defensive characteristics.

The broader narrative is shifting.

Markets are no longer reacting to isolated events. They are adjusting to a world where multiple risks, geopolitical, economic, and financial, are converging at once.

Source:ASX Market Data, March 23, 2026; Global market data; AMP, ANZ, J.P. Morgan commentary

What is your take on this story?

Disclaimer - Skrill Network is designed solely for educational and informational use. The content on this website should not be considered as investment advice or a directive. Before making any investment choices, it is crucial to carry out your own research, taking into account your individual investment objectives and personal situation. If you're considering investment decisions influenced by the information on this website, you should either seek independent financial counsel from a qualified expert or independently verify and research the information.